The “Phantom Loss” Strategy for High Earners

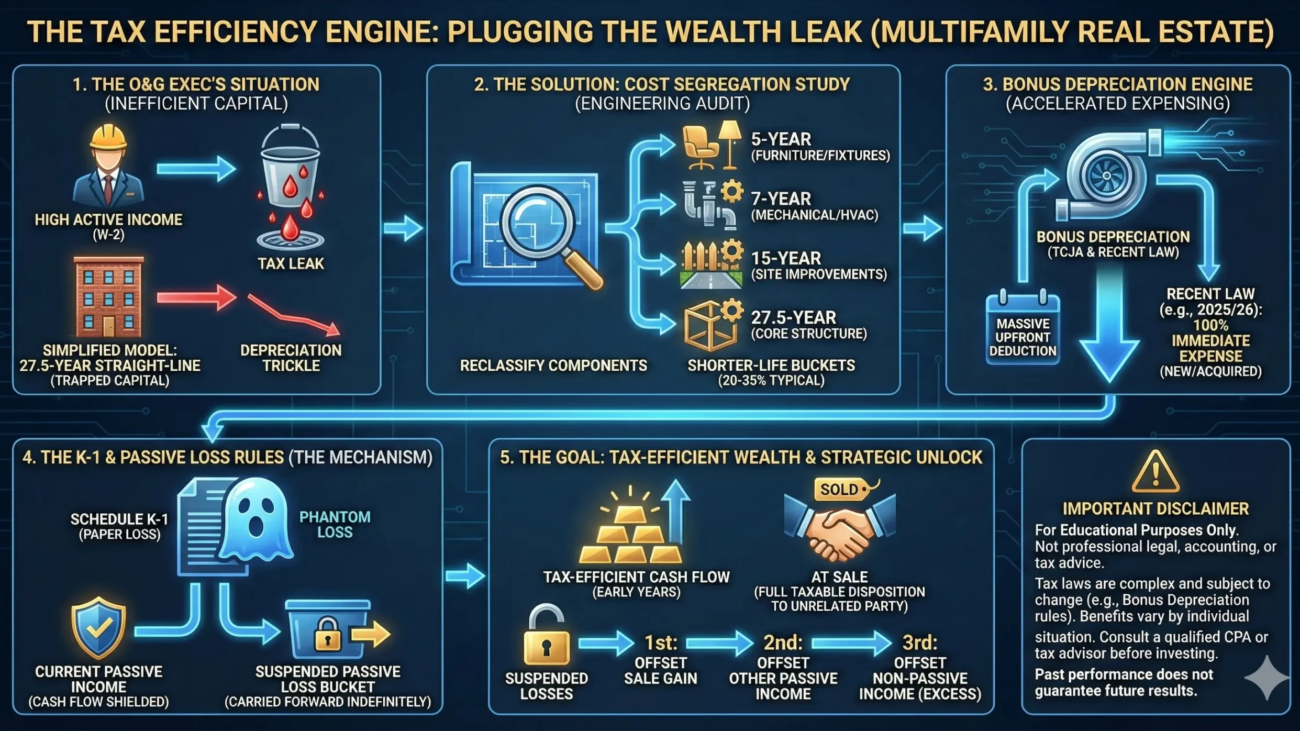

For high-net-worth executives in the Oil & Gas sector, tax mitigation is not merely a convenience; it is a critical component of wealth preservation. You are likely already familiar with sector-specific mechanisms such as Intangible Drilling Costs (IDCs) and the percentage depletion allowance. These Congress-enacted tools are essential for de-risking significant capital expenditures in exploration and production.

Institutional-grade multifamily real estate offers a parallel—and arguably more powerful—tax mechanism utilized by sophisticated family offices and wealth managers: Cost Segregation combined with Bonus Depreciation.

While tax rules allow for shorter recovery periods for specific property components, many smaller or passive investors effectively treat an entire residential property as a single 27.5-year “building” asset for simplicity. This often leads to an inefficient use of capital, as tax-saving potential is trapped within the structure for nearly three decades. Best practice in institutional asset management involves treating the property not as a single block, but as an assembly of distinct industrial components, each with its own specific useful life as defined by the IRS.

What is a Cost Segregation Study?

A Cost Segregation Study is a technical, forensic engineering-based audit of a commercial property. While there is no explicit statutory requirement that only engineers perform these studies, IRS guidance identifies detailed engineering-based studies as best practice for establishing the legal and physical basis for accelerated depreciation.

The objective is to reclassify assets that would normally be effectively claimed over 27.5 years (residential) or 39 years (commercial) into shorter recovery periods—specifically 5, 7, and 15-year asset classes. The legal basis for these studies rests on seminal tax court cases (such as Hospital Corporation of America v. Commissioner) and specific IRS revenue procedures. By properly identifying and documenting these components, a significant portion of the building’s purchase price—often in the range of 20%–35% depending on the property type—can be shifted into shorter-life classes.

The engineering team assigns values to components such as:

- 5-Year Property: Carpeting, specialized lighting, dedicated electrical outlets for equipment, cabinetry, and removable fixtures.

- 7-Year Property: Certain telecommunications equipment and office furniture.

- 15-Year Property: Land improvements like sidewalks, paving, curbing, fences, landscaping, and storm sewers.

The Engine of Efficiency: Bonus Depreciation and Recent Law Changes

Identifying these shorter-life assets is only the first step. The true power of this strategy lies in Bonus Depreciation, which allows investors to immediately expense a large percentage of an asset’s cost in the year it is placed in service. Under the Tax Cuts and Jobs Act (TCJA), this benefit applies to both new construction and acquired (used) properties, provided the property is “new to the taxpayer” and meets the specific acquisition requirements under IRC 168(k).

As of early 2026, it is critical for investors to recognize that the bonus depreciation landscape has evolved beyond the original TCJA phase-out schedule. While the original law saw percentages drop from 100% in 2022 down to 40% in 2025, subsequent legislation (often referred to as the “One Big Beautiful Bill”) has restored 100% bonus depreciation for qualifying property placed in service after January 19, 2025. Property placed in service earlier in 2025 may be subject to different treatment.

Because tax law is currently nuanced and subject to recent legislative adjustments, investors must confirm the exact applicable percentages for their specific acquisition date with a qualified CPA.

Comparison: Simplified vs. Component-Based Depreciation

The following table illustrates how identifying specific components unlocks faster recovery.

| Component Type | Simplified/Small Investor Model | Component-Based (Cost Segregation) Model |

| Core Structure (Walls, Roof, Foundation) | 27.5 Years (Straight Line) | 27.5 Years (Straight Line) |

| Mechanical/HVAC Components | Effectively 27.5 Years | 5 – 7 Years (Eligible for Bonus) |

| Site Improvements (Parking, Landscaping) | Effectively 27.5 Years | 15 Years (Eligible for Bonus) |

| Furniture/Fixtures/Specialty Electric | Effectively 27.5 Years | 5 Years (Eligible for Bonus) |

The Engineering of a K-1: Navigating Passive Loss Rules

The practical outcome of this strategy is experienced when the investor receives their IRS Schedule K-1. While an asset may be producing real monthly cash flow, the K-1 may show a substantial net loss for tax purposes due to the heavy depreciation expense taken. For many investors, these deductions can significantly reduce or even eliminate taxable income from the investment in early years, depending on their broader passive income picture and current law.

The Passive Bucket and “Suspended Losses”

The IRS generally categorizes income into three buckets: Active/Earned (W-2), Portfolio (Stocks/Dividends), and Passive (Rental Real Estate). For high-income executives, passive losses typically cannot offset W-2 salary or stock dividends in the current year. While a limited “active participation” exception exists that allows for a modest rental loss offset, this phases out at higher income levels and typically does not benefit the high-income O&G professional.

However, if these losses exceed your passive income, they become Suspended Passive Losses, which are carried forward indefinitely.

The Strategic Unlock at Sale

Upon the fully taxable disposition of an investor’s entire interest in a passive activity to an unrelated party (under IRC 469(g)), any remaining suspended losses associated with that specific activity are “unlocked.” Following IRS ordering rules, these losses are first applied against the gain from the sale of that activity, then against other passive income. If losses remain after these steps, the excess may then be treated as non-passive and used to offset other types of income.

The Goal: Achieving Tax-Efficient Cash Flow

The strategic objective is to engineer a scenario where investors receive positive cash-on-cash returns that are shielded from federal income taxes during the initial years of ownership. This isn’t a “loophole”—it is the disciplined application of the tax code to encourage infrastructure investment.

IMPORTANT DISCLAIMERS

The information provided in this article is for educational and informational purposes only and should not be construed as professional legal, accounting, or tax advice. Neither Anchorstone Investments nor its principals are licensed CPA firms or tax attorneys. Tax laws, particularly those regarding Bonus Depreciation and the “One Big Beautiful Bill,” are highly complex, nuanced, and subject to ongoing legislative changes, IRS interpretations, and court rulings.

Individual tax situations vary significantly. The benefits of these strategies depend on numerous factors, including an investor’s adjusted gross income, other sources of passive income, and specific acquisition dates. Investors MUST consult with their own qualified CPAs or tax advisors to confirm current law and determine how these strategies apply to their specific financial situation before making any investment decisions.